China’s energy landscape has undergone dramatic transformation over the past two decades, with oil consumption patterns reflecting the nation’s rapid economic growth and evolving energy needs. The relationship between China’s oil demand and domestic production reveals critical insights into one of the world’s most significant energy markets and its implications for global oil dynamics.

As the world’s second-largest economy and most populous nation, China’s energy consumption patterns have far-reaching consequences for international oil markets, geopolitical relationships, and global energy security. The data spanning from 2007 to 2025 illustrates a compelling narrative of sustained demand growth coupled with production challenges that have reshaped China’s position in the global energy ecosystem.

The Strategic Importance of Oil in China’s Economy

Oil remains a cornerstone of China’s energy security strategy, despite increasing emphasis on renewable energy sources and electric vehicle adoption. The transportation sector, petrochemical industry, and manufacturing base continue to drive substantial oil consumption, making energy security a national priority. Understanding the divergence between domestic production capabilities and consumption requirements is essential for analyzing China’s foreign policy decisions, trade relationships, and economic planning.

Data Sources and Methodology

The analysis presented in this article draws from authoritative sources including the International Energy Agency (IEA) for demand forecasting and the U.S. Energy Information Administration (EIA) for production data. These organizations employ rigorous methodologies for data collection and analysis, providing reliable benchmarks for understanding market trends and making informed projections about future developments.

The Relentless Rise of Oil Demand

Exponential Growth Trajectory

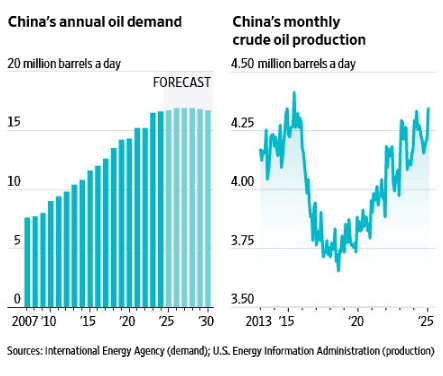

China’s oil demand has demonstrated remarkable consistency in its upward trajectory, growing from approximately 7 million barrels per day in 2007 to forecasted levels approaching 16 million barrels per day by 2025. This represents more than a doubling of consumption over an 18-year period, reflecting average annual growth rates that have consistently outpaced most developed economies.

The demand curve shows particularly steep growth during the 2010-2020 decade, coinciding with China’s rapid urbanization, expanding middle class, and infrastructure development boom. Even during periods of global economic uncertainty, including the 2008 financial crisis and the COVID-19 pandemic, China’s oil demand has shown resilience and continued growth, albeit with occasional temporary plateaus.

Driving Forces Behind Demand Growth

Several interconnected factors have fueled China’s insatiable appetite for oil. The transportation sector has been a primary driver, with vehicle ownership rates increasing dramatically as disposable incomes rose and urbanization accelerated. The development of highway systems, expansion of logistics networks, and growth in commercial transportation have all contributed to sustained demand growth.

Industrial demand has remained robust, particularly from the petrochemical sector, which serves as a foundation for manufacturing industries ranging from plastics to synthetic materials. The construction boom that characterized much of China’s development over this period required significant energy inputs, including oil-derived products for equipment operation and materials production.

Economic Implications of Rising Demand

The continuous upward trajectory of oil demand has profound implications for China’s economic planning and fiscal policy. Higher oil consumption translates directly into increased import requirements, affecting the trade balance and foreign exchange reserves. Energy costs represent a significant component of production costs across multiple industries, influencing competitiveness in international markets.

The predictable nature of demand growth, as evidenced by the smooth upward trajectory in the data, has enabled long-term energy planning and strategic resource allocation. However, it has also created vulnerabilities related to supply disruptions and price volatility in international oil markets.

Production Challenges and Market Dynamics

The Production Reality

While China’s oil demand has followed a remarkably consistent upward path, domestic crude oil production tells a more complex story. Monthly production data reveals significant volatility, with output fluctuating between approximately 3.5 and 4.5 million barrels per day throughout the analyzed period. This volatility contrasts sharply with the steady demand growth and highlights the challenges facing China’s domestic oil industry.

The production data shows several distinct phases: a period of relative stability around 4.0-4.2 million barrels per day from 2013 to 2015, followed by a notable decline to lows around 3.7 million barrels per day in the 2016-2018 period. Subsequently, production has recovered and shown signs of growth, reaching levels above 4.2 million barrels per day in recent years.

Technical and Geological Constraints

China’s oil production challenges stem from several technical and geological factors. Many of the country’s major oil fields are mature, experiencing natural decline rates that require increasingly sophisticated and expensive extraction techniques to maintain output levels. Enhanced oil recovery methods, while effective, significantly increase production costs and technical complexity.

The geographical distribution of China’s oil resources also presents logistical challenges. Major producing regions are often located far from primary consumption centers, necessitating extensive transportation infrastructure and adding to overall supply chain costs. Weather conditions, particularly in northern regions, can impact production operations and contribute to the monthly volatility observed in the data.

Investment and Technology Considerations

Maintaining and expanding oil production requires substantial capital investment in exploration, drilling, and production infrastructure. The cyclical nature of oil markets affects investment decisions, with companies often reducing exploration and development spending during low-price periods, leading to future production constraints.

Technological advancement has played a crucial role in China’s efforts to maximize domestic production. Implementation of advanced drilling techniques, digital monitoring systems, and enhanced recovery methods has helped offset natural field decline rates. However, these technologies require ongoing investment and expertise, contributing to the overall cost structure of domestic production.

The Growing Import Dependency Gap

The divergence between demand and production creates an ever-widening gap that must be filled through imports. In 2007, the gap between demand and production was approximately 3-4 million barrels per day. By 2025, this gap is projected to exceed 11 million barrels per day, representing one of the world’s largest oil import requirements.

This growing dependency on imports has transformed China into a major player in global oil markets, with purchasing decisions and strategic relationships significantly influencing international oil prices and trade flows. The import dependency also creates vulnerabilities related to supply security and price volatility, driving China’s efforts to diversify supplier relationships and develop strategic petroleum reserves.

Strategic Implications and Future Outlook

Energy Security Imperatives

The widening gap between oil demand and domestic production has elevated energy security to a central position in China’s national security strategy. Import dependency exceeding 70% creates vulnerabilities that extend beyond economic considerations to encompass geopolitical and strategic dimensions. This reality has driven China to pursue diversified supplier relationships, develop alternative transportation routes, and invest in strategic petroleum reserves.

China’s Belt and Road Initiative can be partially understood as an energy security strategy, creating economic partnerships and infrastructure connections with oil-producing regions. Investments in pipeline infrastructure, port facilities, and refining capacity in partner countries represent efforts to secure long-term energy supplies and reduce dependence on potentially vulnerable maritime transport routes.

Market Impact and Global Implications

China’s position as a major oil importer provides significant market influence, with demand fluctuations and purchasing decisions affecting global oil prices. The predictable growth trajectory of Chinese demand has provided stability for international oil markets, offering producers reliable demand forecasts for long-term planning.

However, any significant changes in China’s economic growth patterns, energy policies, or consumption trends could have profound implications for global oil balances. The transition toward electric vehicles, industrial efficiency improvements, and renewable energy adoption could potentially alter the demand trajectory, creating ripple effects throughout international energy markets.

Policy Responses and Adaptation Strategies

Chinese policymakers have implemented various strategies to address the challenges posed by growing import dependency. Strategic petroleum reserve development has accelerated, with storage capacity expansion aimed at providing buffer capacity against supply disruptions. Diversification of import sources has reduced dependence on any single supplier region, enhancing supply security.

Investment in alternative energy sources and energy efficiency technologies represents a long-term strategy to moderate oil demand growth. Electric vehicle promotion, industrial energy efficiency standards, and renewable energy development all contribute to efforts to reduce the rate of oil demand growth, though absolute consumption levels continue to rise.

Future Scenarios and Uncertainties

Looking beyond 2025, several factors could influence the trajectory of China’s oil demand and production balance. Economic growth patterns, urbanization rates, and transportation sector evolution will all play crucial roles in determining future energy requirements. Climate policies and carbon reduction commitments may accelerate the transition away from oil in certain sectors.

Technological developments in domestic oil production, including unconventional resource development and enhanced recovery techniques, could potentially increase domestic output. However, geological constraints and environmental considerations may limit the extent of production growth from domestic sources.

Conclusion

The data presented illustrates the fundamental challenge facing China’s energy sector: managing the tension between rapidly growing oil demand and constrained domestic production capacity. This challenge has transformed China into a pivotal player in global oil markets while creating strategic vulnerabilities that influence foreign policy, economic planning, and energy security strategies.

The consistent growth in demand, coupled with volatile but constrained domestic production, ensures that China will remain a major force in international oil markets for the foreseeable future. Understanding these dynamics is essential for energy market participants, policymakers, and analysts seeking to navigate the complex landscape of global energy security and market dynamics.

The path forward will require continued adaptation, strategic planning, and innovative approaches to balance energy security imperatives with economic development objectives and environmental commitments. China’s experience offers valuable insights into the challenges facing major energy-consuming nations in an interconnected global economy.