he American corn industry stands at a fascinating crossroads in 2025. Two seemingly contradictory trends have emerged that tell a deeper story about modern agriculture, global markets, and the forces reshaping how America feeds itself and the world.

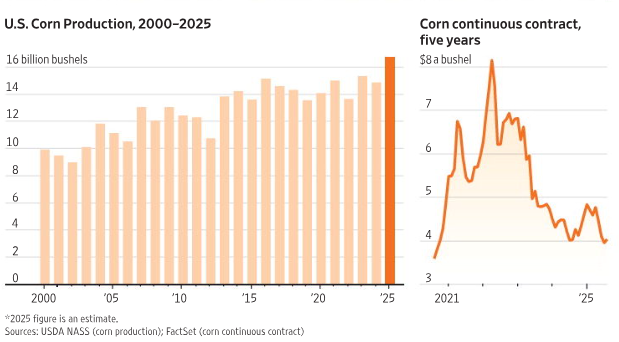

On one hand, U.S. corn production has reached unprecedented heights, with the 2025 harvest estimated at approximately 15 billion bushels—a remarkable achievement that represents decades of agricultural innovation. On the other hand, corn futures prices have plummeted from their 2021 peak of nearly $8 per bushel to hover around $4 per bushel today, a dramatic 50% decline that has profound implications for farming communities across the heartland.

These twin narratives—abundance and declining value—capture the complex dynamics of contemporary agriculture. They reflect technological breakthroughs in farming, shifting global trade patterns, changing energy policies, and the eternal challenge farmers face: the more efficiently they produce, the more they can undermine their own profitability.

The Production Miracle

The left chart reveals a production story that would astound farmers from previous generations. From 2000 to 2025, U.S. corn production has grown substantially, moving from roughly 10 billion bushels at the turn of the millennium to an estimated 15 billion bushels in 2025. This isn’t just incremental growth—it represents a 50% increase in output over a single generation.

This production surge stems from a revolution in agricultural technology. Modern precision agriculture uses GPS-guided tractors, drone surveillance, and soil sensors that optimize every aspect of planting and cultivation. Genetic improvements have created corn varieties that resist drought, pests, and disease while producing higher yields per acre. Farmers can now extract more bushels from the same land their grandparents worked, sometimes doubling or tripling historical yields.

The consistency of high production levels since 2010 is particularly notable. With few exceptions, the U.S. has sustained production above 13 billion bushels annually for the past fifteen years. The slight dip in 2025 compared to the record-breaking years of 2023-2024 may reflect normal weather variations or adjustments in planted acreage, but the overall trend line points unmistakably upward.

This productivity boom extends beyond technology. Improved farming practices, better crop rotation strategies, and advances in fertilizer application have all contributed. The American Midwest has essentially become a highly optimized corn-production machine, capable of feeding livestock, producing ethanol, and supplying global markets with remarkable efficiency.

The Price Collapse

While production has soared, the right chart tells a more sobering story. Corn futures prices peaked dramatically in 2021, briefly touching nearly $8 per bushel—a price level that brought both celebration and concern to farming communities. For farmers who had already planted and could lock in those prices, it represented windfall profits. For livestock producers and food manufacturers who depend on affordable corn, it signaled rising costs throughout the supply chain.

Since that 2021 peak, prices have undergone a prolonged decline, settling into a range around $4 per bushel by 2025. This represents a return to more historical norms, but the journey downward has been painful for many agricultural stakeholders. The volatility visible in the chart—the sharp peaks and valleys from 2021 through 2023—reflects a market trying to find equilibrium amid rapidly changing conditions.

Several factors drove the 2021 price spike. The COVID-19 pandemic had disrupted global supply chains and created unusual demand patterns. Extreme weather in key growing regions temporarily reduced yields. Strong export demand, particularly from China, tightened available supplies. Additionally, the ethanol industry’s appetite for corn as a renewable fuel source kept domestic demand robust.

The subsequent decline reflects a market correction as these temporary factors resolved. Production recovered and even exceeded previous levels. Global competitors, particularly Brazil and Argentina, expanded their own corn production. Chinese demand moderated as their economy slowed and they diversified feed sources. The ethanol sector faced headwinds from changing energy policies and increased competition from electric vehicles.

The Paradox of Agricultural Abundance

The juxtaposition of these two charts illustrates one of agriculture’s fundamental paradoxes: success in production doesn’t necessarily translate to economic success for producers. When everyone produces bumper crops simultaneously, abundance becomes its own problem.

This phenomenon, sometimes called the “treadmill of production,” has plagued agriculture for generations. Individual farmers have strong incentives to maximize yields—more bushels per acre means more income per acre. But when every farmer succeeds simultaneously, the collective abundance drives down prices. Farmers find themselves running faster just to stay in place, producing more but earning less per unit.

The situation is compounded by corn’s nature as a commodity. Unlike branded consumer products, one farmer’s corn is essentially identical to another’s. Farmers can’t charge premium prices based on marketing or brand loyalty. They’re price takers, not price makers, vulnerable to the impersonal forces of supply and demand.

The economic pressure created by this paradox forces continuous consolidation in American agriculture. Larger farms with greater efficiency can survive on thinner profit margins. Smaller operations often struggle when prices decline, leading to the steady disappearance of mid-sized family farms. The average age of American farmers continues to rise as younger generations find it increasingly difficult to enter a profession where success in growing crops doesn’t guarantee financial stability.

Global Forces at Play

Understanding these trends requires looking beyond American borders. Corn production and pricing exist within a complex global ecosystem where events halfway around the world can dramatically impact Iowa farmers.

Brazil has emerged as a major corn producer and competitor to the United States. Brazilian farmers have aggressively expanded production, taking advantage of lower land costs and favorable weather. When Brazilian production surges, it eases global supply constraints and puts downward pressure on prices. The U.S. no longer enjoys the market dominance it once did.

Chinese demand remains a critical variable. As the world’s largest pork producer, China needs vast quantities of corn to feed pigs. Changes in Chinese livestock herds, trade policies, or economic growth directly impact global corn markets. The African swine fever outbreak that devastated Chinese pig populations in 2019-2020, followed by aggressive herd rebuilding, created the volatile demand patterns visible in the price chart.

Geopolitical events matter too. Russia’s invasion of Ukraine in 2022 disrupted global grain markets, as Ukraine is a major corn exporter. Sanctions, shipping disruptions, and uncertainty about Black Sea exports initially drove prices higher but also encouraged other producers to fill the gap. The global system proved more resilient than many anticipated, contributing to the eventual price decline.

Climate change introduces growing uncertainty. While farmers have adapted remarkably well to changing conditions, the increasing frequency of extreme weather events—droughts, floods, unexpected freezes—creates volatility in both production and prices. A severe drought in the American Midwest could quickly reverse the downward price trend, while record harvests elsewhere could push prices even lower.

The Ethanol Factor

No discussion of American corn markets is complete without addressing ethanol. Since the Energy Policy Act of 2005 and the subsequent Renewable Fuel Standard, corn-based ethanol has consumed a massive share of U.S. corn production—often 40% or more of the total crop.

This policy transformed corn from primarily an animal feed and food ingredient into an energy commodity as well. Ethanol plants sprung up across the Midwest, providing a guaranteed domestic market for corn and supporting prices. The ethanol boom contributed significantly to the production increases visible in the chart, as farmers responded to strong demand by planting more acres.

However, the ethanol sector now faces headwinds. The rise of electric vehicles threatens to reduce gasoline consumption over time, potentially decreasing ethanol demand. Environmental questions about corn ethanol’s actual carbon footprint have sparked policy debates. Some argue that producing corn for fuel competes with food production and isn’t as sustainable as once believed.

Changes in ethanol demand could significantly impact future corn prices. If the ethanol industry contracts, farmers would need to find alternative markets for billions of bushels currently consumed by fuel production. Export markets and livestock feeding couldn’t easily absorb that volume without substantial price declines. Conversely, new uses for corn—perhaps in bioplastics or other industrial applications—could provide support.

Looking Ahead: What the Future Holds

As we look beyond 2025, several scenarios could unfold. The most likely path involves continued production efficiency gains but persistent price pressure from global competition and abundant supplies. Farmers will need to manage costs carefully, as profit margins remain thin.

Consolidation in farming will likely continue. Larger operations with access to the latest technology, better financing, and greater bargaining power will expand. Small and mid-sized farms will face difficult choices about whether to grow, exit agriculture, or find niche markets that command premium prices.

Climate adaptation will become increasingly critical. As weather patterns shift and extreme events become more common, farmers will need crop varieties and practices that handle greater variability. Water availability may become a limiting factor in some traditional growing regions.

Policy decisions will shape outcomes. Farm bill provisions, crop insurance programs, trade agreements, and energy policies all influence the economics of corn production. Political debates about agricultural subsidies, environmental regulations, and international trade will determine the framework within which farmers operate.

Technology continues to advance rapidly. Genetic editing tools like CRISPR could create corn varieties with unprecedented characteristics. Artificial intelligence might optimize farm management in ways currently unimaginable. Vertical farming and controlled environment agriculture, while unlikely to replace traditional corn farming, could impact certain markets.

The challenge for American agriculture is transforming production success into economic sustainability. Growing record crops is impressive, but farmers ultimately need profitable crops. Finding that balance—between abundance and value, between efficiency and sustainability, between feeding the world and sustaining farming communities—remains agriculture’s central challenge as we move deeper into the 21st century.