Introduction to the Housing Market Trends

The U.S. housing market has experienced significant volatility over the past five years, driven by a combination of economic policies, inflation, and shifting buyer behavior. Two key indicators—median existing-home price changes and 30-year fixed mortgage rates—tell a story of rapid growth, sharp declines, and a challenging recovery. This article explores the interplay between these metrics from 2020 to 2025, examining their impact on homebuyers, sellers, and the broader economy.

In 2020, the housing market entered a period of unprecedented growth, fueled by low mortgage rates and a surge in demand. However, as rates began to rise and economic conditions shifted, the market faced new challenges. By May 2025, with mortgage rates at 6.8% and home price growth at 2.7% year-over-year, the landscape looks vastly different. Let’s dive into the data to understand what’s driving these trends.

The Surge in Home Prices (2020–2022)

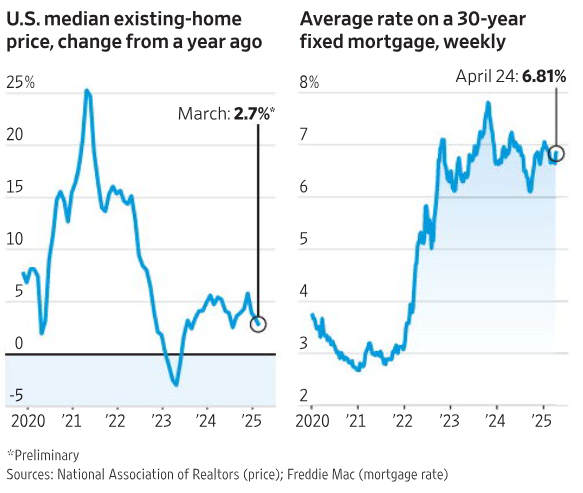

The first graph in our analysis (to be inserted here) illustrates the year-over-year change in U.S. median existing-home prices from 2020 to 2025. Between 2020 and early 2022, home prices soared, peaking at a staggering 20% year-over-year increase. This surge was driven by a combination of factors: historically low mortgage rates, a limited supply of homes, and heightened demand as remote work prompted many to seek larger living spaces.

During this period, the Federal Reserve maintained near-zero interest rates to support the economy through the COVID-19 pandemic. This made borrowing cheap, encouraging buyers to enter the market. However, the lack of housing inventory—exacerbated by construction delays and homeowners reluctant to sell—created a supply-demand imbalance that pushed prices to record highs. For many Americans, homeownership became increasingly out of reach, with affordability hitting its lowest levels in decades.

The Mortgage Rate Rollercoaster

The second graph (to be inserted here) tracks the average rate on a 30-year fixed mortgage over the same period. Starting at around 3% in 2020, rates remained low through 2021, fueling the home price boom. However, by 2022, inflation began to spike, prompting the Federal Reserve to raise interest rates aggressively to cool the economy. This shift is reflected in the graph, with mortgage rates climbing steadily and peaking at 6.8% by April 24, 2025.

The rapid rise in rates had a profound impact on the housing market. Higher borrowing costs reduced affordability, slowing buyer demand and putting downward pressure on home prices. The graph shows a brief dip in rates in 2023, likely due to temporary economic uncertainty, but the upward trend resumed as inflationary pressures persisted. By 2025, the 6.8% rate—while not the highest in history—marked a significant increase from the sub-3% rates that buyers enjoyed just a few years earlier.

The Price Correction and Market Cooling

Returning to the home price graph, we see a dramatic shift starting in mid-2022. As mortgage rates climbed, the year-over-year price growth plummeted, dipping into negative territory by late 2022 and early 2023. This marked the first significant price correction since the Great Recession, with median home prices declining by as much as 5% year-over-year. The combination of high interest rates and economic uncertainty—coupled with inflation eroding purchasing power—deterred buyers, leading to a cooling market.

For sellers, this period was challenging. Homes sat on the market longer, and bidding wars became less common. However, the correction was not as severe as some feared. The graph shows that by 2024, price growth stabilized, hovering around 0% before gradually recovering. By March 2025, the year-over-year price change had returned to a modest 2.7%, signaling a cautious recovery. This suggests that while the market faced headwinds, underlying demand for housing remained resilient.

The Interplay Between Prices and Rates

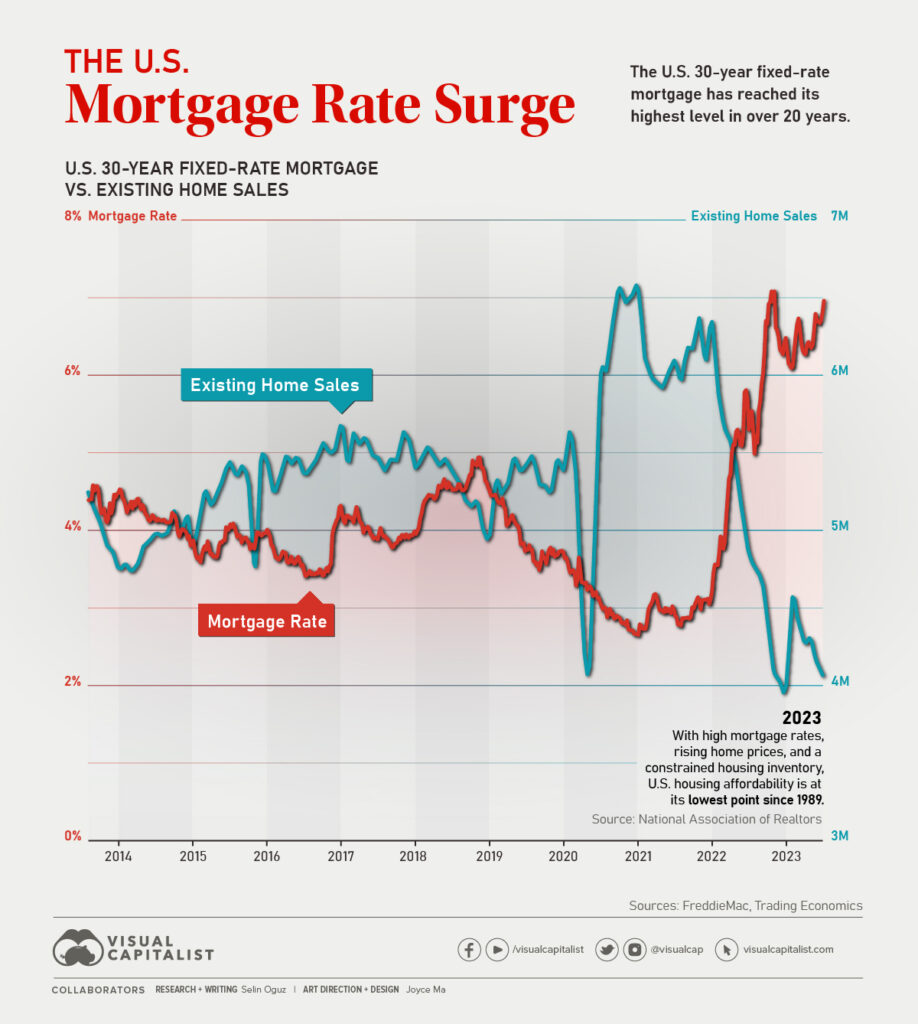

The relationship between home prices and mortgage rates is a critical one. When rates are low, as they were in 2020–2021, borrowing is more affordable, driving up demand and, consequently, home prices. Conversely, when rates rise, as they did from 2022 onward, affordability decreases, cooling demand and putting downward pressure on prices. The graphs illustrate this dynamic clearly: the peak in home price growth in 2021–2022 coincided with the lowest mortgage rates, while the price correction in 2023 aligned with the sharpest rate increases.

By 2025, the market appears to be finding a new equilibrium. At 6.8%, mortgage rates are high enough to keep price growth modest but not so high as to completely stall the market. The 2.7% year-over-year price increase in March 2025 suggests that buyers are adapting to the higher-rate environment, possibly due to wage growth, pent-up demand, or a gradual increase in housing supply. However, affordability remains a challenge, particularly for first-time buyers, who face both high prices and elevated borrowing costs.

Looking Ahead: What’s Next for the Housing Market?

As we move further into 2025, the housing market faces an uncertain but cautiously optimistic future. The Federal Reserve’s efforts to combat inflation have stabilized the economy to some extent, but high mortgage rates are likely to persist unless significant policy shifts occur. For home prices, the modest 2.7% growth in March 2025 suggests a slow but steady recovery, though a return to the double-digit growth of 2021 seems unlikely in the near term.

For prospective buyers, the current market offers both challenges and opportunities. While high rates and prices remain barriers, the cooling of the market has reduced competition, giving buyers more negotiating power. Sellers, meanwhile, may need to adjust expectations, as the days of rapid price appreciation are behind us for now.

In conclusion, the U.S. housing market from 2020 to 2025 has been a rollercoaster of highs and lows, driven by the interplay of home prices and mortgage rates. The data (as shown in the graphs) highlights the market’s sensitivity to economic conditions and underscores the importance of affordability in shaping housing trends. As we look ahead, a balanced approach to monetary policy, combined with efforts to increase housing supply, will be key to ensuring a stable and accessible market for all Americans.