Foreign investors have plenty of reasons to be wary of U.S. government debt at the moment. Now there is another: They can often receive better returns buying bonds in their own countries.

The risk of a weaker U.S. dollar and the cost of protecting against that risk, are making American assets less attractive around the world. That comes at a bad time for the U.S. Treasury market, which is already contending with a darkening U.S. budget picture and the trade war.

Foreign investors likely don’t fear a U.S. default or anything close. But the premium many once received for buying U.S. debt, thanks to higher long-term rates here, has disappeared.

This is happening because short-term rates have stayed high in the U.S. relative to those in the rest of the world, and the Federal Reserve looks less likely to cut them anytime soon.

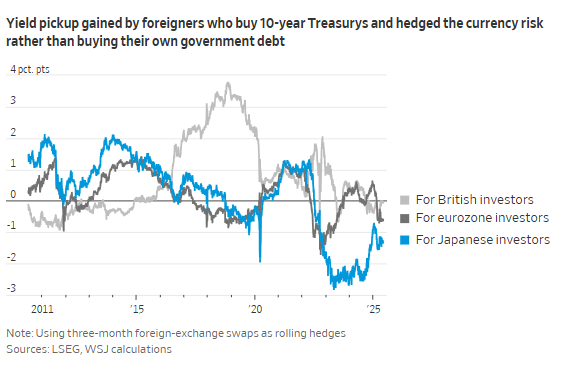

When institutional investors buy foreign-currency assets, they must hedge this risk or face potential losses from exchange-rate moves. This is why, for major U.S. debt buyers in the eurozone and Japan, 10-year Treasury yields of around 4.5% aren’t necessarily attractive, even if their own government bonds offer just 2.5% and 1.5%, respectively. What matters is the return after hedging dollar fluctuations. Since 2008, this pickup has often justified the trade.

That is no longer true. British investors switching from U.K. government bonds to Treasurys receive no premium after hedging. Eurozone buyers experience a post-hedged yield difference of minus 0.6 percentage point compared with Germany’s 10-year government bonds and even worse versus other European bonds.

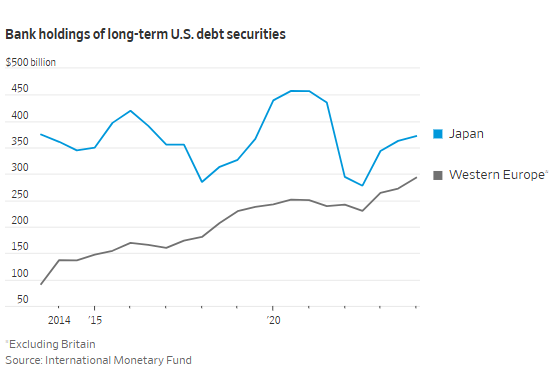

While Japanese banks, pension funds and insurers could have theoretically bought more U.S. debt and clipped the bigger coupons, the rise in hedging costs, driven by the Fed’s pushing up short-term rates, was much steeper. This led them to dump $331 billion of it instead, according to International Monetary Fund data.

If they stoke inflation, the Fed might cut rates at a slower pace. Anticipation of this has led to a flatter yield curve in the U.S., just as it steepens in the eurozone, Britain and Japan.

This matters for currency-hedged returns: Investors hedge long-term bonds using short-term derivatives—typically three-month foreign-exchange swaps, which are highly liquid—making it an implicit bet on the relative shape of yield curves.