The recent leap in longer-term U.S. Treasury yields has unnerved investors. But it could play into the hands of the country’s lenders.

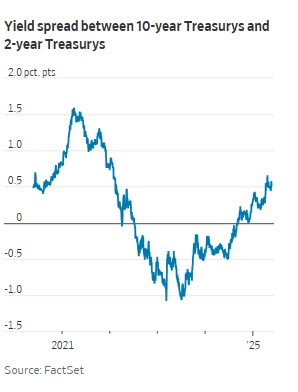

This means shorter-duration securities, such as those that mature in a matter of months, are yielding less than longer-duration ones. The difference in what 2-year and 10-year Treasurys yield recently has been around its biggest since 2022.

For years, the curve had been fairly flat. That meant yields were roughly the same at different maturities, or even inverted, with shorter-term yields higher than longer-term ones. Those were challenging curve shapes for the core business of banking.

Banks get the bulk of their funding in the short-term market, in the form of deposits. Payouts on those are mostly linked to very short-term rates.

Then they either lend out or invest these funds, typically in longer-term assets such as loans, mortgage bonds or long-dated Treasurys. The difference between the rates at which they borrow and lend is their profit, also referred to as their net interest margin.

So even if the short-term picture for the U.S. economy is muddied by tariffs, concern over long-term deficit expansion and inflation could actually fuel an improving dynamic for banks’ core lending profits.

Improving net interest margins, which have been below their longer-term levels, could help buffer some of the other headwinds banks face. These include fears that a trade war could tip the U.S. economy into recession.

There is a flip side to this. When long-term rates rise, the value of bonds bought at lower yields declines.

Rising long-term yields can also have a capital benefit in the near term. As older bonds mature, the cash can be rolled over into new, higher-paying bonds.

That means bank assets generate more income, which can be retained as capital. If the Trump administration also takes actions that lower banks’ capital requirements, it would leave banks with even more excess capital than they already have. This could cover some forced selling of bonds in a liquidity crunch.

It could also give banks greater flexibility to increase their lending if the economy grows, or add to buybacks if loan demand isn’t materializing.

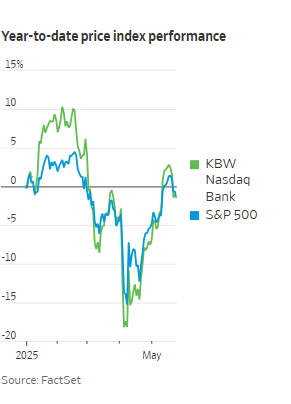

The market has been unsure of what to do with banks this year. Early in 2025, bank stocks outperformed the broader market on hopes for a stronger economy. They mostly underperformed in March and April when tariff fears dominated. At the moment, the KBW Nasdaq Bank Index and the S&P 500 are both almost flat for the year.

If the yield curve continues to steepen at a moderate pace, that could put some wind back into the sails of bank stocks.