No wonder high-dividend funds are hot. In July and August, as investors became more convinced interest rates will fall, exchange-traded funds specializing in dividend-paying stocks took in $4.5 billion in new money.

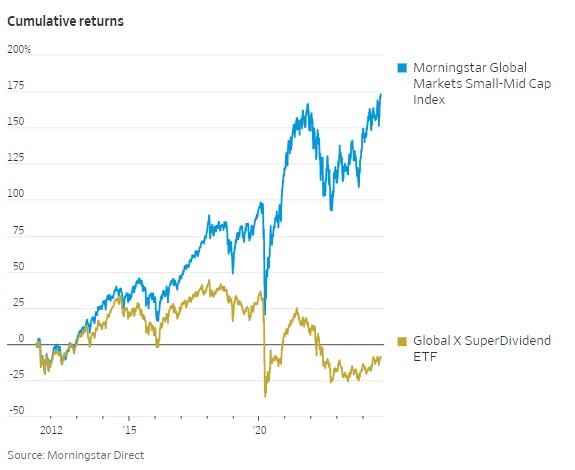

The SuperDividend fund’s supersized yield comes at a cost. Launched in June 2011 at $75, this week the shares traded around $22. That’s a 70% decline.

If you’d bought the ETF at its inception and held continuously through the end of August, you’d have lost 9%—after accounting for all those jumbo dividends along the way. Although the fund slightly outperformed its own benchmark of high-yielding companies, it lagged far behind global small and midsize stocks as a whole.

A company that pays a steady stream of growing dividends is probably in robust financial health, but one that pays gigantic dividends is probably struggling and may be desperate to attract investors. Put a bunch of those into an ETF, and you get lots of income but even more risk.

According to Morningstar, 17 ETFs with combined assets of $10.3 billion yield at least 6%. Among them: three other SuperDividend funds from Global X, two funds from First Trust and two from Invesco.

High-dividend funds often hold many more energy and financial stocks than broader portfolios do. That can raise risk.

Invesco KBW High Dividend Yield Financial is yielding a stratospheric 11.9%. Its average holding has a market value of only $2 billion. More than 40% of its assets are in mortgage real-estate investment trusts, which borrow money to invest in home loans and mortgage-backed securities.

Since its launch in December 2010, the fund has returned an annual average of 6.7%, including dividends. Its larger sibling, Invesco KBW Bank, has gained an average of 11.5% annually over the same period, also including dividends—even though its yield, at 2.8%, is paltry by comparison.