Utility bills are getting expensive and catching the attention of politicians. That means unpleasant surprises could be building up for utility investors.

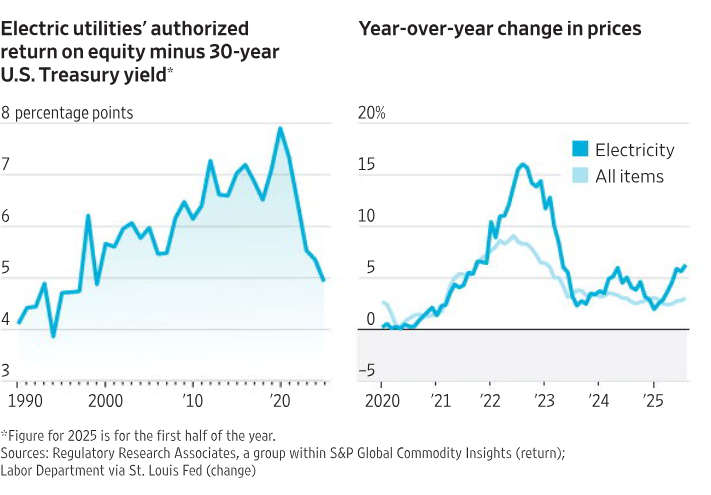

Power prices have been rising faster than inflation for the past few years. Electricity prices in August were 31% higher than four years earlier, compared with about 19% for prices overall, according to data from the Labor Department.

Data centers’ increasing power needs are partly to blame, but so are overdue investments to upgrade aging parts of the grid and costs associated with replacing old coal-fired power plants. Inflation for inputs from steel to labor all contribute to higher electricity bills.

In New Jersey, the two gubernatorial candidates have made rising electricity bills key talking points of their campaigns. Earlier this year, New York and Rhode Island introduced bills proposing to cap utilities’ allowed return on equity at 4%. By comparison, electric utilities nationwide have historically on average been allowed to earn around 10%, according to data from S&P Global Commodity Insights.

The allowed return is supposed to reflect the cost of capital, or the return that investors require to buy utilities’ stocks. Utilities tend to pay out a big chunk of their earnings on dividends rather than retaining it, which means they rely on equity raises to fund investments. Energy think tank Rocky Mountain Institute estimated that the return on equity accounts for 15% to 20% of customers’ bills.

The return hurdle is a subjective measure, though. A return that seemed fair when customers’ utility bills were rising slowly could start to look excessive when those bills suddenly skyrocket. Utility regulators tend to be elected or appointed by elected officials, so they aren’t immune to political pressure.

Despite the utility sector’s reputation as a stable, boring sector, artificial intelligence’s high demand for power has brought some enthusiasm to the sector. Electric utilities in the S&P 500 are up about 14% year to date, slightly outperforming the overall index. Their shares as a multiple of forward earnings are about 16% more expensive than the 20-year average.

Squabbles between utilities and consumer advocates aren’t new, but they are likely to get more heated as electricity prices keep climbing. Between newly rising power demand and much-needed upgrades to the grid, power prices seem to have nowhere to go but up.