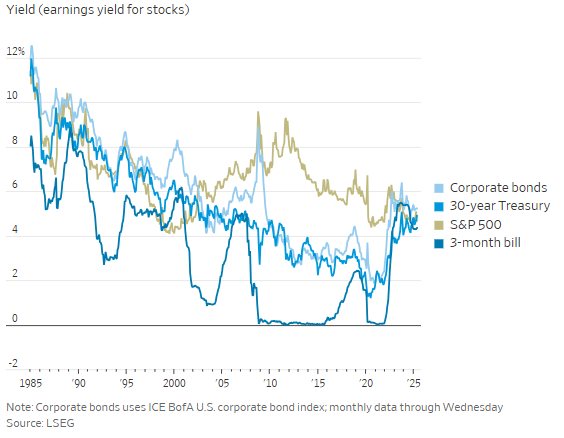

Treasurys, stocks, cash and corporate bonds all yield about the same. Either risky assets are less rewarding than usual or safe assets are less safe than usual.

The gap between the highest and lowest yields among the main U.S. assets is the smallest in 40 years, having dropped after the election in November and stayed low. This uses the earnings yield for stocks, the earnings divided by price, or the inverse of the PE ratio, along with the yields on the three-month Treasury bill, as a proxy for cash, the 10-year and 30-year Treasurys and the ICE BofA U.S. corporate bond index.

How we got here is well known, owing to two things: inflation and profits. Cash and government bond yields have risen back up to something more like the pre-2008 norm thanks to the Federal Reserve’s eventual response to the 2022 inflation spike. High profit margins and bets on earnings growth pushed up the valuation of the S&P 500, lowering the earnings yield, while strong balance sheets reduced the extra yield demanded to lend to big companies.

This convergence made investors a lot of money if they got it right on the way up, choosing stocks over bonds since the pandemic. But it leaves investors with a dilemma. There is little reward for locking up money in long-dated Treasurys instead of a money-market fund or bills. There is little reward for lending to big companies instead of the government. And stocks need to have reached a permanently higher rate of profit growth to justify the much-lower-than-usual extra earnings yield above Treasurys.

Investors have to make two calls. First, are stocks really worth paying 21 times their expected earnings over the next 12 months, an earnings yield of just 4.7%? With 10-year Treasurys at 4.4%, that represents almost no margin of safety. The bet is that earnings increase fast to justify the high valuation—indeed, Wall Street forecasts more than 13% earnings growth next year and the year after, almost double the long-run average and a sharp increase from this year’s 9% prediction.

Second, could it be that the margin of safety stocks have over bonds is actually bigger, because Treasurys now embed more risk? Estimates of the extra yield above future interest rates demanded to lock up money in a 10-year Treasury, known as the term premium, have risen fast in the past couple of years to the highest since 2014. This reflects volatility as much as risk of inflation or default, but it is still a risk.

This avoids the issue of similar yields on everything in the U.S. by looking at assets that haven’t yet converged: stocks elsewhere. Luca Paolini, chief strategist of Pictet Asset Management, says a “great convergence” is coming between the growth of the U.S., China, Europe and Japan. To profit from it, steer clear of expensive U.S. stocks and the dollar, and look for bargains in Europe and Japan.

The convergence he is focused on results from faster economic growth in Europe and Japan and slower growth in the U.S. and China. Japan has already shaken up its staid corporate sector and seems to have broken the deflationary mindset. Germany has abandoned fiscal austerity and plans to pump money into the economy, and the European Commission is at least talking about deregulation.

The U.S. slowdown is already under way, and the combination of tariff barriers and weaker immigration should slow it further. China’s growth should slow naturally as it gets richer, even without the continued real-estate crisis.

European and Japanese stocks this year, in dollar terms, has reduced the U.S. premium a bit. But Big Tech is all based in the U.S., and still rolling in cash, and the U.S. economy is still likely to grow much faster.