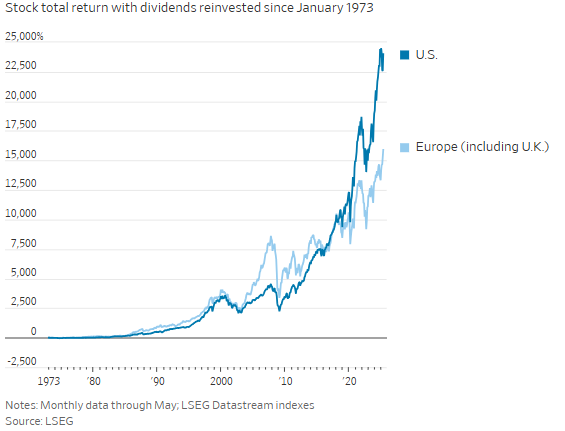

It’s easy to think of Europe as the investment that time forgot. Even after this year’s strong performance, European investments have lagged far behind the U.S. for the past decade and more.

But it would be wrong to regard Europe as having been a disaster forever: Look backward, and it matched American stock returns for decades before the euro crisis and the rise of Big Tech in the U.S.

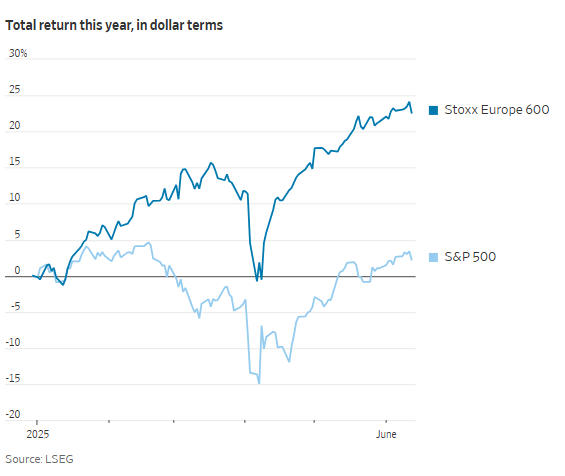

Investors might question the current mania for investing outside the U.S., when stocks in the rest of the world gained 14% this year against the U.S.’s 2% (about half of the rest of the world’s gain was due to the plunging greenback—all figures in dollar terms).

But too many people focus on the dismal returns since 2010, when the Greek crisis began, and forget that once Europe was a viable investment alternative. The scary stat: Since 2010 the S&P 500 is up more than 500%. European stocks are up less than 150%. The reminder: In the previous 15 years, from 1995, the S&P made only 130% while Europe gained 220%.

Europe’s failure to keep up with emerging tech shows up in big U.S. companies having far higher profit margins than big European ones. Among smaller companies, though, profit margins are about the same.

Strip out the skew toward the biggest by putting equal weight on each S&P stock—rather than putting more weight on the more valuable, as the basic index does—and U.S. and European returns were roughly the same from the end of 2021 until the November election. It isn’t so much U.S. exceptionalism, as Mag7 exceptionalism.

Yet, the difference isn’t all about Big Tech. Europe’s economy has been sluggish ever since its currency crisis of the early 2010s, while inflexible labor law combined in some cases with political pressure meant companies were slow to cut back on capacity. The result is less intense use of factories and other assets, meaning an even bigger advantage for U.S. return on investment than the gap in margins implies.

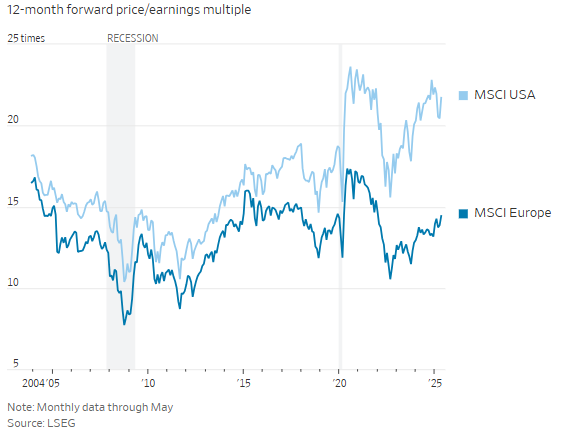

These differences were compounded from 2017 onward by a sharp rise in U.S. valuations that wasn’t matched in Europe. Again, this was about the biggest companies; U.S. smaller companies trade at a premium to Europe, but about the same as they always have.

On the economy, Europe has decided for the first time since the euro crisis that it needs to let rip with government spending. Germany is leading the way, plowing money into defense and infrastructure, which ought to reflate its economy—and help lift corporate capacity utilization and profits. The European Central Bank has been cutting rates, too, though higher energy costs after Israel’s strike on Iran might give it pause.

The trade-off confronting investors: The U.S.’s biggest stocks are more innovative and profitable but also far more expensive, while Europe’s are much less interesting but are cheap and have stimulus, plus an appeal to investors looking to diversify away from their highly concentrated U.S. holdings.

Europe just has to close the performance gap with the U.S. a little to make it an interesting investment—again.