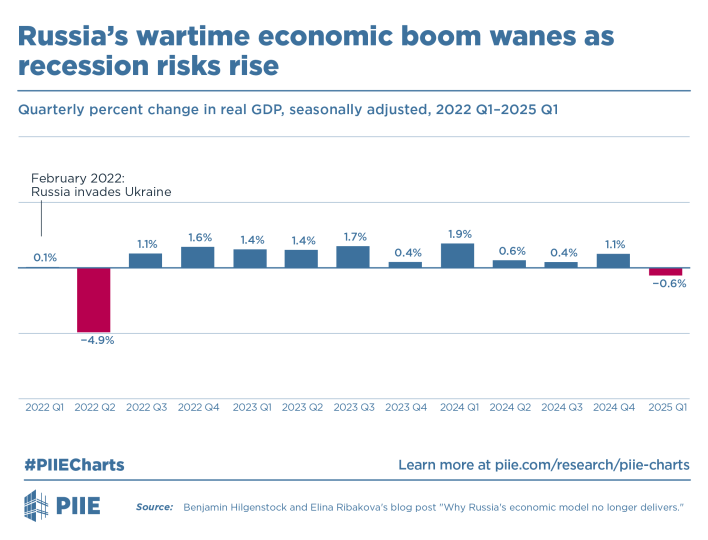

The Russian economy has undergone dramatic shifts since the onset of the war in Ukraine in February 2022. The invasion sparked a period of extreme volatility, with an immediate contraction in GDP followed by a surprising rebound fueled by wartime spending and resource exports. However, as the chart provided by the Peterson Institute for International Economics (PIIE) illustrates, this boom is beginning to wane. By early 2025, signs of economic slowdown and potential recession have emerged, raising questions about the sustainability of Russia’s wartime economic model.

This article analyzes Russia’s quarterly GDP performance from Q1 2022 to Q1 2025, highlighting the initial collapse, subsequent recovery, and the eventual weakening growth pattern. It also examines the driving factors behind these shifts, such as sanctions, military expenditures, global energy markets, and structural challenges within the Russian economy.

The Initial Shock and Rapid Recovery

In Q2 2022, immediately after the invasion of Ukraine, Russia’s GDP contracted sharply by nearly 5%. This was largely the result of unprecedented Western sanctions, capital flight, and the disruption of trade. Many predicted a prolonged collapse of the Russian economy.

However, starting in Q3 2022, the economy rebounded more strongly than expected. Growth of 1.1% in Q3, 1.6% in Q4, and steady gains into 2023 reflected the government’s rapid shift toward a war economy. Several factors contributed to this rebound:

- Military Spending: Massive state expenditure on defense production provided jobs and industrial demand.

- Energy Exports: Despite sanctions, Russia continued exporting oil and gas, often redirecting flows to Asia, particularly China and India.

- Import Substitution: Restrictions on Western goods encouraged domestic production and increased reliance on non-Western suppliers.

The Peak and Emerging Weaknesses

The peak of Russia’s wartime boom came in late 2023 and early 2024, when quarterly GDP growth reached as high as 1.9% in Q4 2023. This growth was largely unsustainable, built on heavy state spending and short-term adjustments in trade flows.

By 2024, cracks began to appear:

- Declining Energy Revenues: Global oil prices stabilized, and discounts on Russian oil exports reduced income.

- Sanction Fatigue: Sanctions on technology, finance, and logistics began to bite harder, limiting investment and modernization.

- Labor Shortages: Mobilization efforts and migration of skilled workers reduced labor market efficiency.

- Inflationary Pressures: Increased government spending without corresponding productivity gains fueled inflation.

The data shows growth slowing in 2024, with gains dropping to just 0.6% in Q2, 0.4% in Q3, and a modest rebound of 1.1% in Q4.

Outlook for 2025 and Beyond

The first quarter of 2025 marked a turning point, with Russia’s GDP contracting by 0.6%. This signals that the wartime boom is giving way to stagnation and possible recession. Unlike in 2022, when recovery was swift, the current slowdown may be more persistent, given structural weaknesses.

Looking ahead:

- Sustainability of Military Spending: Continuous high defense spending is unsustainable without cutting other social and economic programs.

- Dependence on China and India: Over-reliance on a limited set of trade partners exposes Russia to external vulnerabilities.

- Innovation Deficit: With limited access to Western technology, Russia faces challenges in diversifying beyond commodities.

- Recession Risks: The contraction in Q1 2025 could deepen if energy revenues fall further or if sanctions tighten.

In conclusion, while Russia demonstrated resilience in the early years of the war, its economic model appears to be reaching its limits. The wartime boom provided temporary stability but has not addressed the deeper structural problems. Without reforms or easing of geopolitical tensions, Russia risks entering a period of prolonged stagnation or recession.