The SAF Revolution Takes Flight

The aviation industry stands at a critical juncture in its history, facing unprecedented pressure to reduce its environmental impact while maintaining the connectivity that drives global commerce and human connection. At the heart of this transformation lies sustainable aviation fuel (SAF), a promising solution that could significantly reduce the carbon footprint of air travel without requiring wholesale changes to existing aircraft infrastructure.

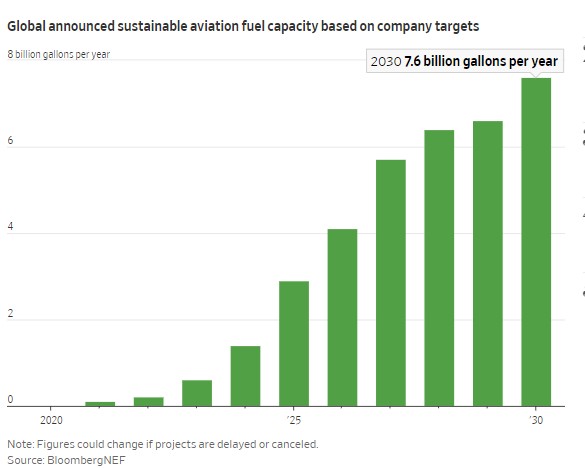

Recent data from BloombergNEF reveals a remarkable trajectory for global SAF production capacity, showing announced targets climbing from virtually zero in 2020 to an ambitious 7.6 billion gallons per year by 2030. This exponential growth curve represents more than just numbers on a chart—it signals a fundamental shift in how the aviation industry approaches environmental responsibility and long-term sustainability.

The significance of this projected growth cannot be overstated. Traditional jet fuel accounts for approximately 2-3% of global carbon emissions, and with air travel demand expected to double over the next two decades, the urgency for cleaner alternatives has never been greater. SAF offers a pathway to dramatically reduce these emissions, with some formulations capable of achieving up to 80% lower lifecycle carbon emissions compared to conventional jet fuel.

However, the journey from current minimal production to the ambitious 2030 targets presents both unprecedented opportunities and formidable challenges. The chart’s steep trajectory raises important questions about feasibility, investment requirements, technological readiness, and the coordination needed across multiple industries and governments to achieve these goals.

The growth pattern shown in the data reflects a combination of factors driving SAF development: increasing regulatory pressure, corporate sustainability commitments, technological advances in production methods, and growing investor confidence in the sector. Major airlines have committed to significant SAF purchasing agreements, while governments worldwide are implementing policies and incentives to accelerate production and adoption.

This transformation extends beyond environmental benefits. The SAF industry represents a new economic frontier, creating opportunities for innovation in feedstock development, production technologies, and supply chain optimization. From agricultural waste and algae to captured carbon and renewable electricity, the diversity of potential SAF feedstocks promises to create new revenue streams for farmers, waste management companies, and renewable energy producers.

As we examine this growth trajectory, it’s essential to understand both the promise and the challenges ahead. The announced capacity targets shown in the chart represent intentions and commitments, but translating these announcements into operational production facilities requires overcoming significant technological, financial, and logistical hurdles.

Current State and Market Dynamics

The sustainable aviation fuel landscape today is characterized by rapid evolution and significant investment, yet it remains in the early stages of scaling up to meet ambitious climate goals. Current global SAF production represents less than 0.1% of total aviation fuel consumption, highlighting both the enormous potential and the scale of the challenge ahead.

The exponential growth curve shown in the BloombergNEF data reflects several key market dynamics driving the industry forward. Regulatory frameworks play a crucial role, with policies like the European Union’s ReFuelEU Aviation mandate requiring SAF blending quotas that gradually increase over time. The United States has implemented tax credits and grant programs through the Inflation Reduction Act, while countries like the United Kingdom, Canada, and Japan have established their own SAF mandates and incentive structures.

Corporate commitments form another critical driver of growth. Major airlines have announced ambitious sustainability targets, with many committing to net-zero emissions by 2050. These commitments translate into long-term SAF purchase agreements that provide the demand certainty necessary to justify large-scale production investments. Airlines like United, Delta, and British Airways have signed multi-billion-dollar SAF supply agreements extending into the next decade.

The technology landscape for SAF production is diverse and rapidly evolving. Currently, the most commercially viable pathway is Hydroprocessed Esters and Fatty Acids (HEFA), which converts used cooking oils, animal fats, and other lipid feedstocks into drop-in jet fuel. However, feedstock availability limits the scalability of HEFA production, driving innovation in alternative pathways such as Fischer-Tropsch synthesis, alcohol-to-jet conversion, and power-to-liquids processes.

Investment flows into the SAF sector have accelerated dramatically, with venture capital, private equity, and corporate strategic investors committing billions of dollars to production facilities and technology development. Traditional oil and gas companies are pivoting portions of their operations toward SAF production, bringing significant capital and operational expertise to the sector. Companies like Shell, BP, and TotalEnergies have announced major SAF production investments, while specialized biofuel producers like Neste and Diamond Green Diesel are expanding their aviation fuel capabilities.

Geographic distribution of announced capacity reveals interesting patterns. The United States dominates announced production capacity, driven by favorable policy frameworks and large domestic aviation markets. Europe follows closely, supported by aggressive climate policies and mandates. Asia-Pacific represents a growing opportunity, with countries like Singapore and Japan developing SAF hubs to serve the region’s expanding aviation sector.

Despite this momentum, significant challenges remain. Feedstock availability and cost represent major constraints, particularly for HEFA-based production. Competition from other sectors for limited sustainable feedstocks, such as renewable diesel and biodiesel production, creates pricing pressure and supply limitations. Additionally, the capital intensity of SAF production facilities requires substantial upfront investment with long payback periods, creating financing challenges for many projects.

The gap between announced capacity and actual production highlights the difference between intentions and execution. Many of the projects included in the 2030 projections are still in planning or early development phases, facing regulatory approvals, financing challenges, and technological risks that could delay or cancel projects.

Challenges and Opportunities in Scaling SAF Production

The path from the current minimal SAF production to the ambitious 7.6 billion gallons per year target by 2030 presents a complex web of challenges that must be addressed simultaneously across multiple dimensions. Understanding these obstacles, along with the opportunities they create, is essential for assessing the feasibility of the projected growth trajectory.

Feedstock Constraints and Innovation

One of the most significant challenges facing SAF scaling is feedstock availability and sustainability. Current HEFA production relies heavily on waste oils and animal fats, but these feedstocks are limited in global supply and face increasing competition from renewable diesel and biodiesel producers. The total global supply of these waste and residue feedstocks is estimated at only 15-20 million tons annually, far below what would be required to meet aviation sector demands.

This constraint is driving innovation in alternative feedstock development. Advanced biofuel pathways using agricultural residues, forestry waste, and dedicated energy crops offer greater scalability potential. Companies are developing technologies to convert municipal solid waste, algae, and even captured carbon dioxide into aviation fuel. Power-to-liquids technologies, which use renewable electricity to synthesize fuel from water and CO2, represent perhaps the most scalable long-term solution, though current costs remain prohibitively high.

Technology and Production Challenges

While HEFA technology is commercially proven, alternative SAF pathways face significant technological hurdles. Fischer-Tropsch synthesis requires substantial capital investment and complex operational management. Alcohol-to-jet pathways must optimize conversion efficiency and reduce production costs. Power-to-liquids processes need dramatic cost reductions in renewable electricity and electrolyzer technologies to become commercially viable.

Production scaling also faces infrastructure challenges. SAF production facilities require specialized equipment, skilled operators, and integration with existing fuel distribution systems. Many announced projects are first-of-their-kind commercial facilities, carrying technology and operational risks that could delay deployment or increase costs beyond projections.

Economic and Financial Barriers

The economics of SAF production remain challenging relative to conventional jet fuel. Current SAF prices are typically 2-4 times higher than petroleum-based jet fuel, creating a significant cost burden for airlines and ultimately air travelers. While carbon pricing, mandates, and subsidies help bridge this gap, long-term cost competitiveness requires continued technological improvement and scale economies.

Capital requirements for the announced capacity expansion are enormous. Industry estimates suggest that achieving the 2030 targets would require $75-100 billion in capital investment globally. This level of investment requires coordination between project developers, financial institutions, governments, and end-users to share risks and provide long-term certainty.

Regulatory and Policy Frameworks

The success of SAF scaling depends heavily on supportive and consistent policy frameworks. While current policies provide important incentives, long-term certainty and international coordination remain critical challenges. Different sustainability standards across regions create complexity for global producers and airlines. Carbon accounting methodologies for SAF continue to evolve, creating uncertainty for investment decisions.

Supply Chain and Infrastructure Development

SAF production requires new supply chains connecting feedstock suppliers, production facilities, and distribution networks. Unlike conventional jet fuel production, which is concentrated in large refineries, SAF production may be more distributed, requiring coordination across numerous smaller facilities. Airport fuel infrastructure must accommodate SAF blending and handling, requiring investment and operational changes.

Opportunities in Crisis

These challenges simultaneously create significant opportunities for innovation and value creation. The feedstock constraint is driving breakthroughs in agricultural waste utilization, creating new revenue streams for farmers and waste management companies. Technology development is attracting significant venture capital and corporate investment, creating opportunities for breakthrough innovations that could transform not just aviation but broader energy systems.

The policy support for SAF is creating first-mover advantages for countries and companies that successfully scale production. Regions that develop SAF production capabilities are positioning themselves as exporters to the global aviation market, potentially creating significant economic value and strategic advantages.

Future Outlook and Industry Transformation

The projected growth in sustainable aviation fuel capacity to 7.6 billion gallons per year by 2030 represents more than a quantitative expansion—it signals a fundamental transformation of the aviation industry’s relationship with energy and environmental impact. Achieving these targets would position SAF as a significant component of the global fuel supply, fundamentally altering market dynamics, pricing structures, and competitive advantages across the aviation sector.

Pathway to Commercial Viability

The scale represented in the 2030 projections would enable significant economies of scale in SAF production, potentially driving down costs toward parity with conventional jet fuel. Industry analyses suggest that SAF prices could decrease by 50-70% as production scales and technologies mature. This cost reduction would reduce the economic burden on airlines and passengers while maintaining the environmental benefits.

However, achieving this cost trajectory requires not just increased production volume but also technological improvements across the entire value chain. Next-generation production technologies, more efficient feedstock conversion processes, and optimized supply chains all contribute to cost reduction potential. The learning curve effects from operating multiple commercial-scale facilities will provide valuable operational knowledge that can be applied to future projects.

Geopolitical and Economic Implications

Large-scale SAF production could reshape global energy trade patterns and create new sources of economic value and strategic advantage. Countries with abundant renewable energy resources, sustainable biomass, or advanced technology capabilities may emerge as SAF exporters, similar to current oil and gas trade relationships. This shift could reduce dependence on traditional petroleum-producing regions while creating new forms of energy security based on domestic or allied renewable resources.

The economic impact extends beyond the aviation sector. SAF production creates jobs in agriculture, manufacturing, and technology development. Rural communities benefit from new markets for agricultural residues and dedicated energy crops. The technology development spillovers from SAF innovation can benefit other sectors requiring sustainable fuels, such as shipping and heavy-duty transportation.

Environmental Impact and Climate Goals

If the projected capacity targets are achieved and fully utilized, the environmental impact could be substantial. Using conservative estimates of 50% lifecycle carbon reduction compared to conventional jet fuel, 7.6 billion gallons of SAF could reduce aviation emissions by approximately 35-40 million tons of CO2 annually. This reduction represents roughly 15-20% of current aviation emissions, a significant contribution toward the industry’s net-zero goals.

However, realizing these environmental benefits requires ensuring that SAF production itself follows sustainable practices. Feedstock production must avoid indirect land use change that could offset carbon benefits. Production facilities should utilize renewable energy to maximize lifecycle carbon reductions. Comprehensive sustainability standards and certification systems will be essential to maintain environmental integrity as the industry scales.

Technology Evolution and Innovation Trajectory

The period leading to 2030 will likely see continued technology evolution and cost reduction in SAF production. Power-to-liquids technologies may reach commercial viability, potentially providing unlimited scalability using renewable electricity and captured CO2. Advanced biofuel pathways using engineered microorganisms could improve conversion efficiency and reduce production costs. Integration with renewable energy systems could optimize production timing and reduce energy costs.

Breakthrough innovations in adjacent technologies could also accelerate SAF adoption. Improvements in renewable energy storage, carbon capture and utilization, and synthetic biology could all contribute to more efficient and cost-effective SAF production. The convergence of these technology trends suggests that the 2030 targets may represent just the beginning of a longer-term transformation.

Risks and Uncertainties

Despite the promising trajectory, significant risks remain that could impact the achievement of these targets. Economic downturns, changes in government policies, technology setbacks, or feedstock availability constraints could delay or reduce planned capacity expansions. The capital-intensive nature of SAF projects makes them vulnerable to financing challenges or changes in investor sentiment.

Competition from alternative decarbonization approaches, such as hydrogen aircraft or battery-electric aviation for shorter routes, could reduce SAF demand in specific market segments. However, SAF remains the most viable near-term solution for long-haul aviation, where alternative technologies face significant technical challenges.

Conclusion: A Transformed Industry

The sustainable aviation fuel capacity growth projected through 2030 represents a critical inflection point for the aviation industry. Success in achieving these targets would demonstrate that large-scale industrial decarbonization is possible through coordinated action across governments, companies, and investors. The transformation extends beyond environmental benefits to encompass new economic opportunities, technological innovation, and strategic advantages.

While challenges remain substantial, the momentum behind SAF development suggests that the industry is committed to this transformation. The exponential growth trajectory shown in the data reflects not just optimistic projections but concrete investments and commitments that are already reshaping the aviation fuel landscape. Whether the ambitious 2030 targets are fully achieved or not, the direction of change is clear: sustainable aviation fuel will play an increasingly central role in the future of flight, fundamentally altering how we think about aviation’s environmental impact and economic structure.

The next decade will be crucial in determining whether this transformation can be achieved at the scale and speed required to meaningfully address aviation’s climate impact while maintaining the connectivity that drives global prosperity and human progress.