Who Were the “Trump Losers”?

During Donald Trump’s presidency (2017–2021), certain countries faced economic headwinds due to his “America First” policies, trade tariffs, and shifting geopolitical alliances. For instance:

- Argentina: Trump’s administration imposed tariffs on Argentine steel and aluminum in 2018, exacerbating the country’s economic crisis under then-President Mauricio Macri. The peso plummeted, and foreign investment dried up, making Argentina a poster child for “Trump losers.”

- Colombia: While less directly targeted, Colombia faced indirect pressures from U.S. trade policies favoring domestic energy and agriculture, impacting its export-driven economy.

- South Africa: Trump’s critical tweets about South Africa’s land reform policies and his administration’s focus on U.S. agricultural exports hurt South African markets, particularly in agriculture and mining.

The Turnaround in 2025

Several factors may explain why these “Trump losers” are now stock market winners:

- Post-Trump Policy Shifts: The Biden administration (2021–2025) reversed some of Trump’s trade tariffs and prioritized multilateral trade agreements, benefiting emerging markets like Argentina, Colombia, and South Africa. For example, renewed trade talks with the European Union and China have boosted Argentina’s agricultural exports, driving stock market gains.

- Commodity Boom: South Africa and Colombia, rich in minerals and oil, have benefited from a global commodity price surge in 2025, fueled by post-pandemic recovery and green energy demands. Gold, copper, and coal prices have soared, lifting South African and Colombian equities.

- Investor Rotation: After years of over-investment in U.S. and Canadian markets, institutional investors are rotating capital into higher-growth emerging markets, attracted by undervalued stocks and higher yields in Argentina and Colombia.

- Domestic Reforms: Argentina’s recent economic reforms under President Javier Milei, including deregulation and fiscal austerity, have restored investor confidence, despite initial pain, leading to a 30% YTD stock market surge.

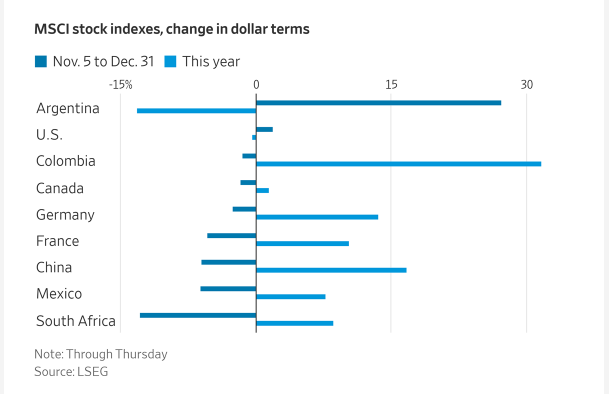

Argentina’s MSCI index performance is the most dramatic, with a 15% drop from November 5 to December 31, followed by a 30% YTD gain. This volatility reflects the country’s economic rollercoaster but also its potential.

Under Trump, Argentina faced punishing tariffs and a U.S.-backed IMF bailout that failed to stabilize its economy. However, by 2025, a combination of Milei’s libertarian policies—cutting subsidies, reducing inflation, and attracting foreign direct investment—has turned the tide. The Buenos Aires stock exchange has seen a rally, driven by energy and agricultural firms benefiting from global demand.

Colombia and South Africa’s Quiet Wins

Colombia and South Africa, with 30% and 15% YTD gains, respectively, are less volatile but equally impressive. Colombia’s oil and coal exports have rebounded, while South Africa’s mining sector—particularly gold and platinum—has capitalized on global demand for critical minerals.

Both nations faced Trump-era challenges, including trade uncertainties and U.S. pressure on commodities. However, post-Trump diplomacy and a focus on sustainable development have revitalized their markets, attracting pension funds and sovereign wealth managers seeking diversification beyond the U.S. and Europe.

What This Means for Investors

For global investors, the rise of “Trump losers” as stock market winners signals a shifting landscape. The U.S. and Canada, once safe havens, are underperforming with minimal YTD gains, while emerging markets offer higher returns but with greater risk.

This trend underscores the importance of geopolitical awareness in portfolio management. Investors who pivoted away from Trump-era losers in 2017–2021 may now regret missing out on Argentina’s 30% surge or Colombia’s steady growth. As of March 2025, diversification into emerging markets could be the key to unlocking alpha in a post-Trump world.

Our opinion

The MSCI stock indices data as of March 6, 2025, paints a surprising picture: the “Trump losers”—Argentina, Colombia, and South Africa—are now the biggest winners in global stock markets. This turnaround reflects a confluence of post-Trump policy shifts, commodity booms, and investor rotations, underpinned by domestic reforms in these nations.

While the U.S. and Canada remain steady, their underperformance highlights a broader rebalancing of global economic power. For investors, policymakers, and analysts, this trend offers a lesson in resilience and the enduring impact of political leadership on financial markets. As we move further into 2025, the story of these “losers turned winners” will likely continue to shape the narrative of global finance.